Thursday, January 8, 2026

Pools from an upcoming bond issuance dominated by closed-end second mortgages originated by loanDepot.com LLC and PennyMac Loan Services LLC carry a notably lower weighted-average coupon even though the underlying collateral lacks the type of credit enhancements that typically accompany lower pricing.

Low coupons define the opening home-equity securitization of the year, as Cerberus Capital Management LP brings a closed-end second mortgage transaction to market with collateral metrics that remain closely aligned with prevailing credit risk standards.

Year-end activity in the home-equity securitization market included a record-setting home-equity investment deal alongside two largely first-lien residential mortgage-backed securities that incorporated limited volumes of junior liens.

A broad dispersion of coupons accompanied three bond issuance featuring loans that fall short of Qualified Mortgage requirements with differing combinations of leverage, borrower credit profiles and cash-flow characteristics.

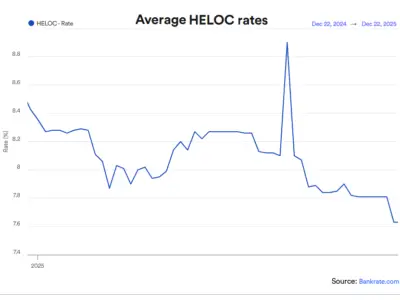

Weighted-average coupons on home-equity line of credit and non-QM bond issuances moved lower in December, while closed-end second and jumbo transactions posted modest increases. More signficant was the quarterly HELOC WAC -- which sank 185 basis points on a year-over-year basis.

Issuance of jumbo residential mortgage-backed securities accelerated into year-end, with a cluster of late-quarter transactions led by affiliates of JPMorgan Chase & Co. and capped by a Goldman Sachs Mortgage Co. deal that closed on the final day of the year.

During 2025, interest rates on open-end home-equity products tumbled nearly three-quarters of a percentage point, while averages on closed-end junior liens dropped by around half that much.

As monthly securitizations of closed-end junior lien and home-equity agreement bonds slipped, open-end issuance surged 43% and skyrocketed 295% from a year earlier. Annual home-equity issuance nearly doubled, with closed-end transactions driving dollar volume higher and open-end deals delivering the largest percentage gain.

By COVIANCE Community home-equity lenders have a timely opportunity—but seizing it requires a more strategic approach. Success will come from moving beyond mass marketing, delivering personalized messaging, and simplifying the borrower experience.

By MICHAEL MICHELETTI Equity-sharing products make up a rising proportion of home-equity originations, and further expansion appears likely as easier equity extraction, intensifying institutional investor demand, and the appeal of having no monthly payment continue to pull more homeowners toward...